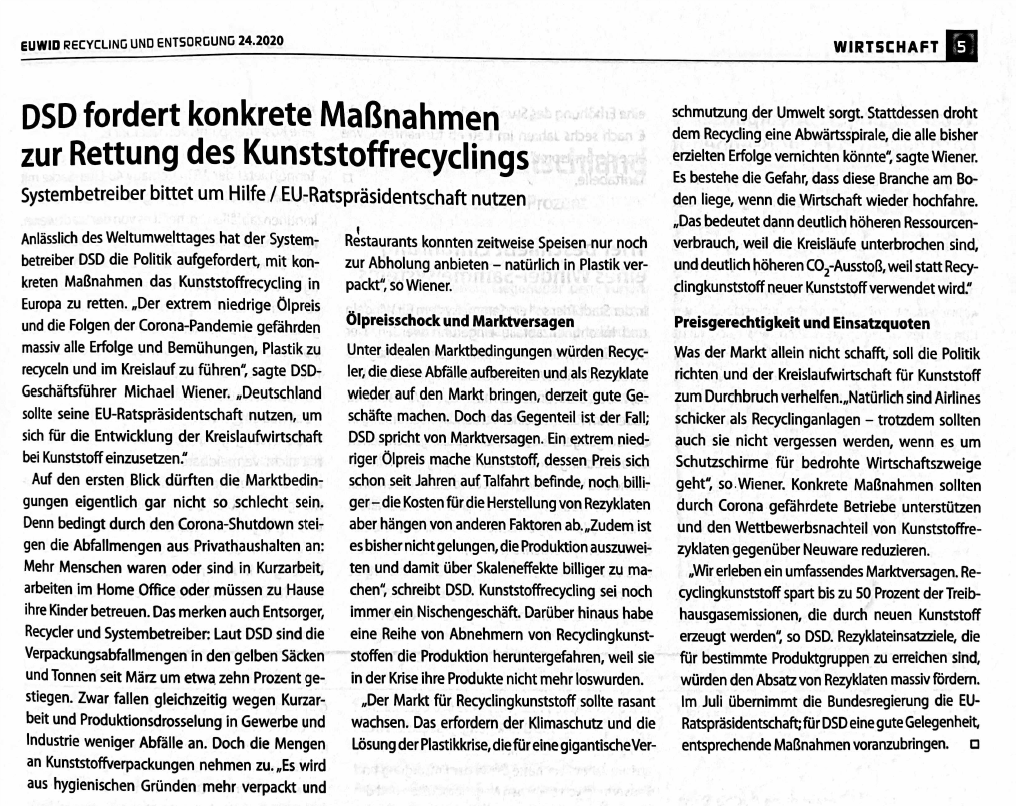

EU leaders have struck a deal on a landmark corona virus recovery package that will involve the European Commission undertaking massive borrowing on the capital markets. Part of this deal is a tax on plastic packaging wastes. Finally good news for the plastic recycling industry!

Read the whole story: By Stefan Baumgarten, 21-Jul-20 17:11

LONDON (ICIS), As part of their €750bn coronavirus pandemic recovery package, EU leaders agreed on a new EU tax on plastic packaging wastes.

The tax, to be introduced as of 1 January 2021, will be calculated on the weight of nonrecycled plastic packaging waste “with a call rate of €0.80/kilogramme with a mechanism to avoid excessively regressive impact on national contributions.” Proceeds from the tax will go to the EU.

German environmental group Deutsche Umwelthilfe (DUH) welcomed the tax, saying it was long overdue. However, DUH said that the tax rate was “too timid”. “We need a price that really causes a change in direction,” said DUH director general Jurgen Resch. “And we need regulations that, above all, end the littering of nature and cities with unnecessary disposable products, be it disposable plastic bottles, plastic bags or disposable coffee-to-go cups,” he said.

Also, instead of basing the tax on the weight of nonrecycled plastic packaging waste, it would be more effective to tax new, virgin primary plastics in packaging as soon as it is put into circulation, DUH said.

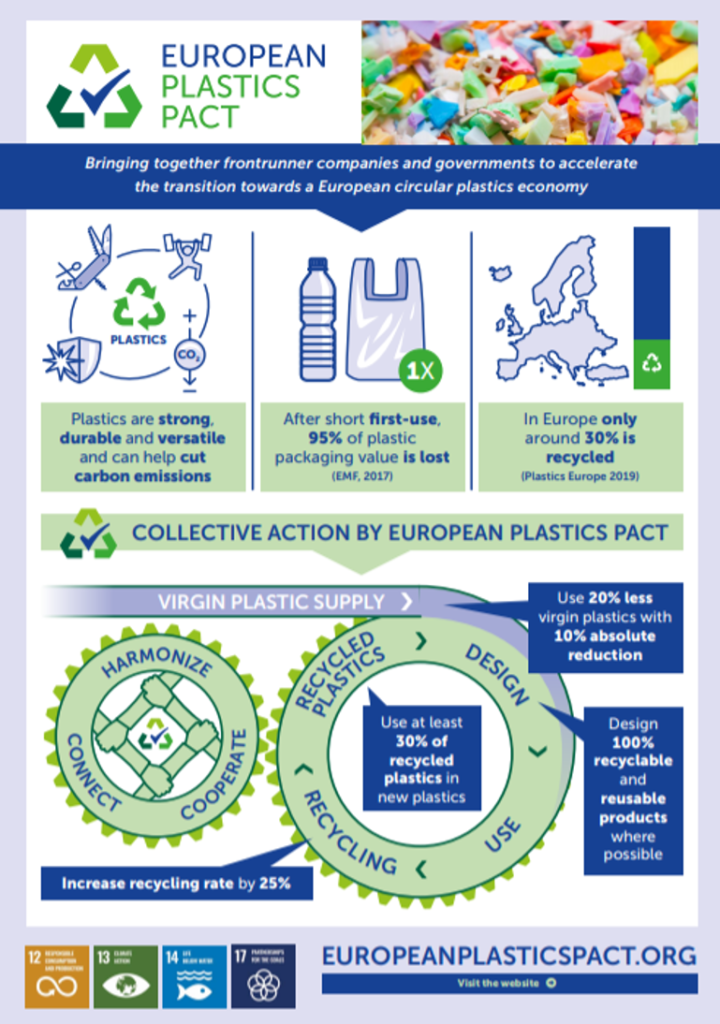

Trade group PlasticsEurope could not immediately be reached for comment. Last week, German chemical producers’ trade group VCI warned against the introduction of EU tax on plastics packaging waste that is not recycled. Legislative measures have driven firms throughout the petrochemical industry and the packaging sector to adopt increasingly ambitious sustainability targets which often go beyond EU mandated minimums.

Many plastic bottle manufacturers are targeting at least 50% recycled material by 2030, or shifting to other materials such as bio-based or non-plastic alternatives which often have a larger environmental impact than plastic because of higher energy usage, CO2 output and weight.

The recycled polyethylene terephthalate (R-PET) chain is perhaps the key example of the extent of the shortage of material because it is currently the most widely recycled plastic in Europe and has the most developed market and infrastructure, Victory said.

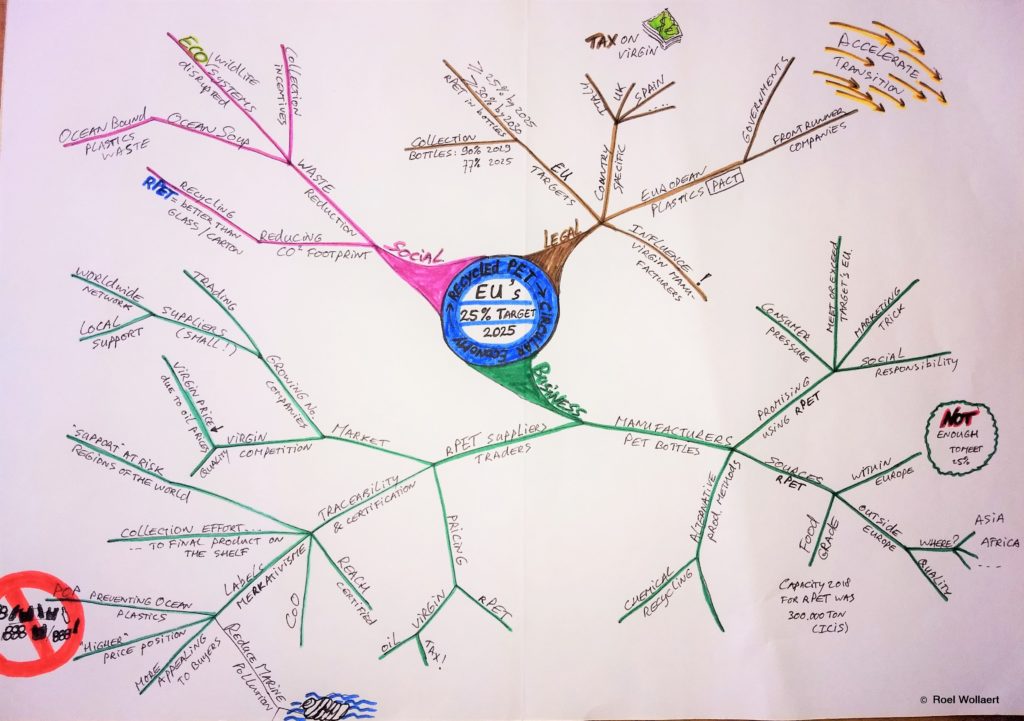

Despite a collection rate of 63% in 2018, the growth rate in collection has slowed at less than 3%/year. ICIS analysis shows to achieve the single-use plastic (SUP) target of 77% the annual growth rate needs to be 9%/year, and this does not even factor in the increasing contamination rates within the region. Cross contamination from other plastics and losses due to the mechanical process, has seen average wastage rates across Europe rise from 25% to around 30-35% according to market estimates.

Other sectors such as fibres and chemical recycling projects are increasingly seeking a higher share of postconsumer polyethylene terephthalate (PET) waste.

Packaging producers using materials such as polyethylene (PE), polypropylene (PP), polystyrene (PS) and polyvinyl chloride (PVC) have also investigated a switch to other materials including PET because of the perception, caused by the headline collection rates, that R-PET material – particularly food-grade material – is in abundant supply.

An additional limit for the plastic bottle market is the lack of food-grade pellet (FGP) production, which currently stands at around 300,000 tonnes/year in Europe, or around 9% of overall PET plastic bottle demand. Coupled with this, to achieve European Food Safety Authority (EFSA) approval, 95% of the material used in reprocessing must have been sourced from food-contact applications, and there must be full and provable traceability throughout the chain.

For R-PET the major feedstock is used plastic drinks bottles, so reaching the 95% threshold is not currently a challenge. But for other recycled material where multiple forms of waste are collected in kerbside schemes, proving provenance of material to reach the 95% content threshold is prohibitive.

For recycled PE (R-PE), for example, the only post-consumer-derived source of food grade pellets is the UK where milk bottles provide an easily separated stream of waste.

The capacity for food grade R-PET is set to increase with limited projects coming on stream into 2021 yet investment is still required to grow capacity at the same rate as demand. FGP usage must triple on 2018 volumes to achieve the SUP 25% target, clearly a challenge for the industry given the pandemic and macroeconomics it faces.

Structural shortages of material, along with technical limitations such as opacity of material and loss of tensile strength, have led companies to explore other avenues for reaching sustainability commitments such as chemical recycling or bio-based materials.